All official European Union website addresses are in the europa.eu domain.

See all EU institutions and bodiesAn official website of the European Union | How do you know?

Environmental information systems

EN

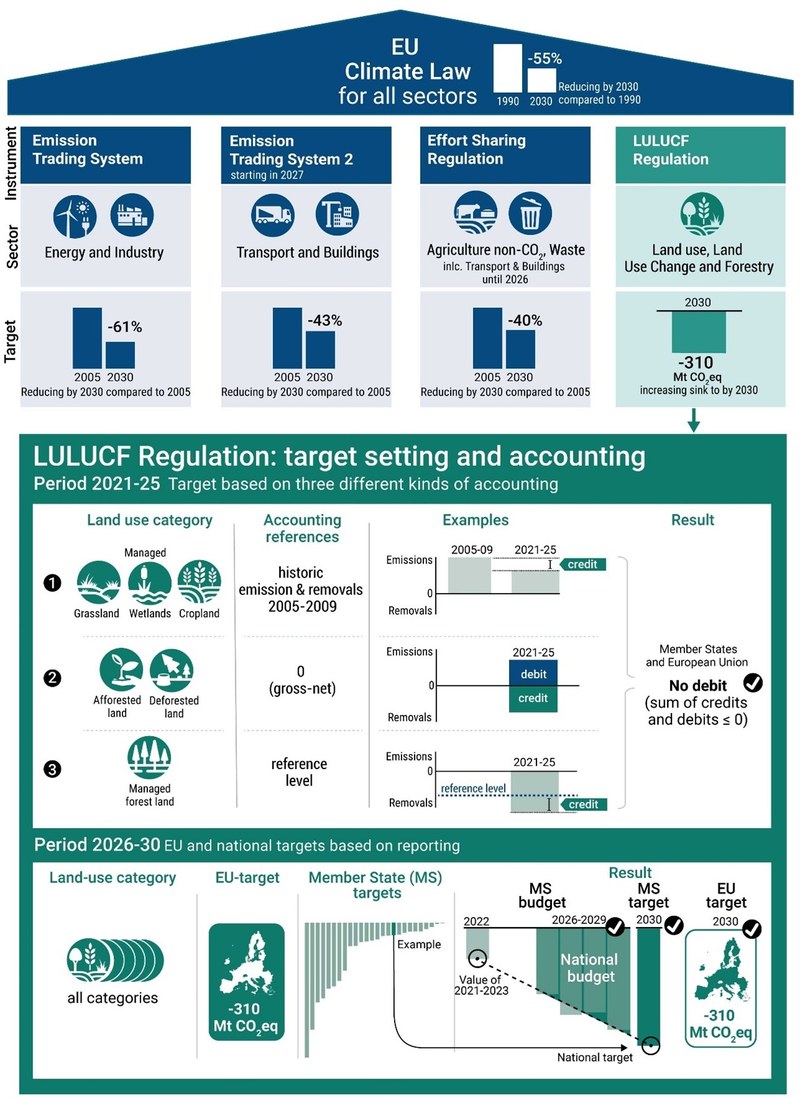

The LULUCF Regulation sets out how land use will contribute to achieving the EU climate targets. The key target is to increase land-based net removals in the EU to -310 Mt CO2eq in 2030.

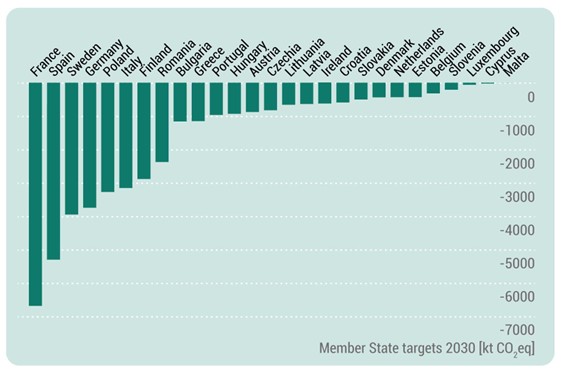

The target is distributed among Member States through individual targets in a way that requires each Member State to increase its climate ambition in their land use policies. There are several flexibilities Member States can make use of under the LULUCF Regulation, both within the sector LULUCF but also with sectors covered by the Effort Sharing Regulation.

Compliance with the targets is assessed through reported data in national GHG inventories. Therefore, robust estimates of annual GHG emissions and removals with high accuracy and timeliness is needed to allow for a reliable assessment of progress towards the targets.

The LULUCF Regulation aims to enhance the accuracy and precision of the Member States’ LULUCF inventories through the application of the IPCC concept of higher Tiers and through an enhanced monitoring of land-use change, using geographically explicit data.

What does the LULUCF Regulation say?

Member State commitments are implemented in two distinct periods. In the period of 2021 to 2025, each Member State needs to comply with the ‘no-debit’ rule. That means they need to ensure that within their LULUCF sector, accounted emissions do not exceed accounted removals.

- In the period of 2021 to 2025, each Member State needs to comply with the ‘no-debit’ rule. That means they need to ensure that within their LULUCF sector, accounted emissions do not exceed accounted removals.

- In the period 2026 to 2030, the accounting towards targets is simplified. The Regulation sets out binding national 2030 targets for each Member State encompassing all emissions and removals in the LULUCF sector reported in GHG inventories. The targets are specified in Annex IIa of the LULUCF Regulation.

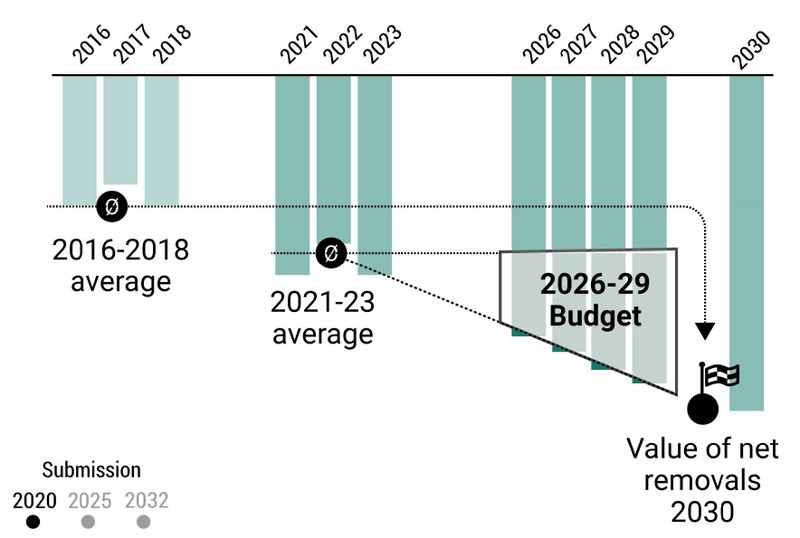

- From 2026 to 2029, there is a ‘budget’ defined as the total aggregate net emissions or removals that are required to reach the target in 2030. In practice, this is defined by a linear trajectory, with a start point in 2022 and end point in 2030.

Compliance with the LULUCF Regulation is assessed in 2027 for the period 2021-2025 and in 2032 for the period 2026-2030. After 2025, the compliance against the targets is assessed directly through the GHG emissions and removals reported in annual GHG inventories that Member States already provide with their reporting obligations under the UNFCCC.

Figure 1: Overview of EU climate policy architecture and Member States’ obligations under the LULUCF Regulation

Source: Own compilation

How are the national targets and budgets set?

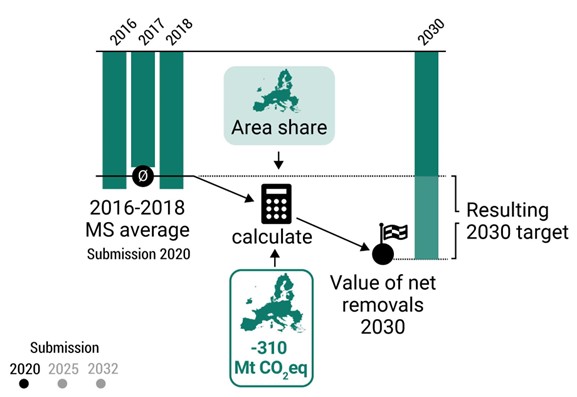

From the Union target to national targets

National budgets

What flexibilities do Member States have for achieving the targets?

There are general flexibilities within the LULUCF sector among Member States and with the ESR.

If a Member State does not meet its LULUCF target or budget, it can deduct annual emission allocations under ESR to LULUCF (Art. 12.1). If a Member State outperforms its LULUCF target and budget, it can transfer its LULUCF remaining overachievement to a Member State that needs it to meet its target (Art. 12.2). It might also use the LULUCF overachievement for compliance under the ESR. This amount is constrained per Member State and for all Member States to a maximum of 50% of 262 Mt CO2eq by the ESR (Art. 7(1), Annex III), for each period (2021 to 2025, and 2026 to 2030).

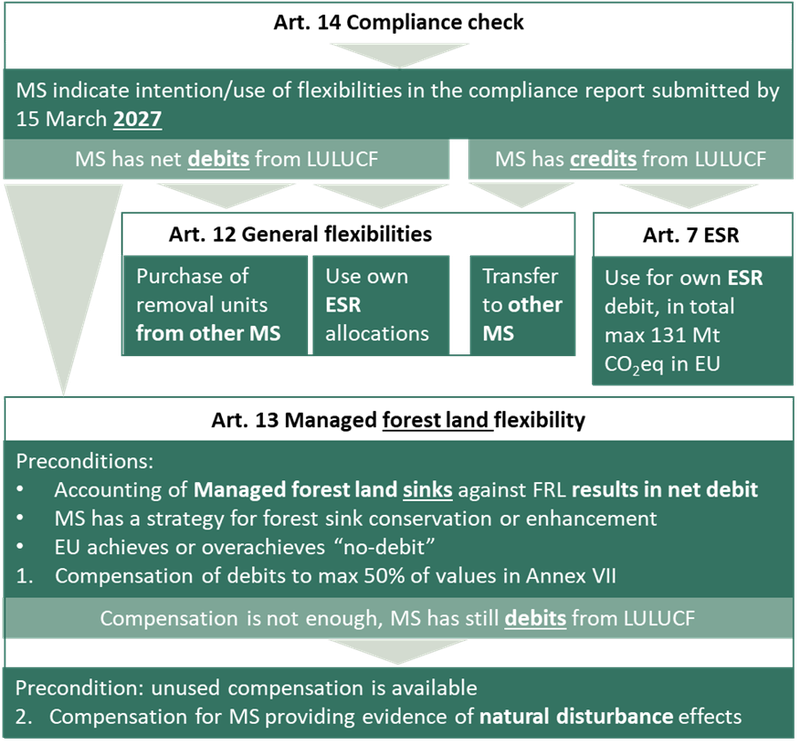

For the years 2021 to 2025 Member States have access to the managed forest land flexibility mechanism (Art. 13).

- If a Member State fails to reach their its ‘no debit’ commitment, managed forest land results in net emissions (debit), that Member State may compensate the forest land debit. A requirement is that the debits results from sinks accounted for as emissions, thus that the country reported a net sink for managed forests provided.

- A requirement is that the debits results from sinks accounted for as emissions, thus that the country reported a net sink for managed forests provided. Another requirement is that the country it has included measures to ensure conservation or the increase in forest sinks in their long-term strategies submitted under the Governance Regulation.

- Finally, the compensation is only allowed if and emissions do not exceed removals in the Union as a whole. In addition granted, the compensation must not exceed 50% of the maximum compensation for the Member State as set out in Annex VII of the LULUCF Regulation.

In the event that a Member State’s total emissions exceed total removals, and after using the compensation attributed to that Member State as set out in Annex VII of the LULUCF Regulation, any remaining emissions may be compensated up to an amount unused by other Member States of the full compensation for the period 2021 to 2025 set out in Annex VII of the LULUCF Regulation. Accessing this flexibility is conditioned upon the submission of evidence to the Commission demonstrating the impact of natural disturbances and the measures to be put in place to avoid or mitigate similar impacts in the future. If the demand for compensation exceeds the unused amount, the compensation will be proportionally distributed among duly justified requests by the Member States concerned.

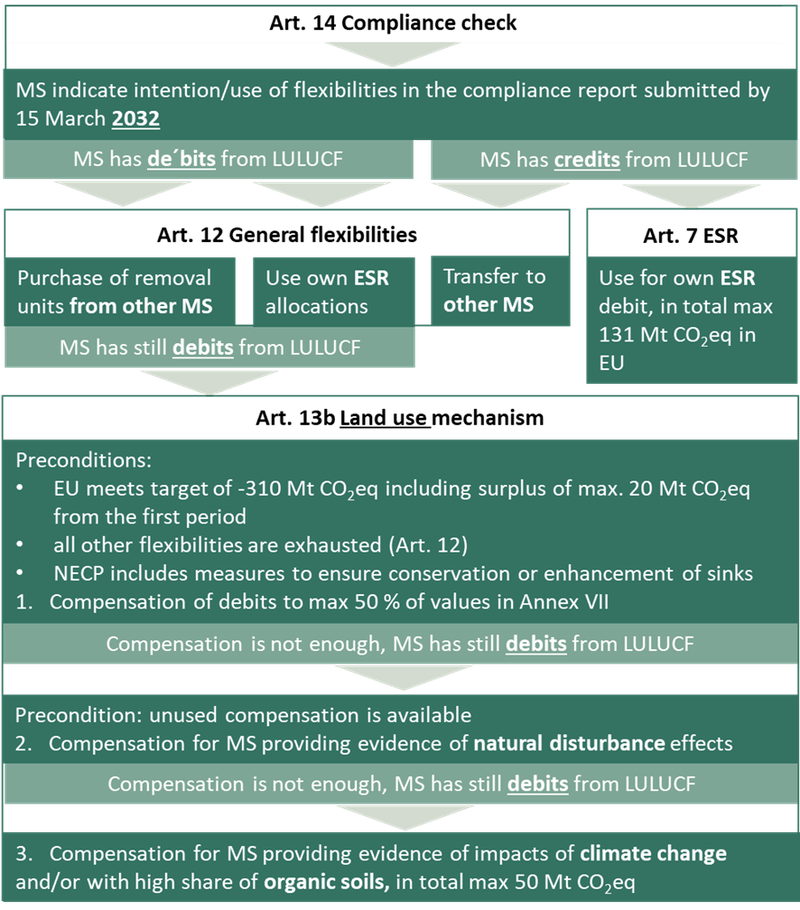

A land use mechanism for the years 2026 to 2030 can be used by Member States that do not meet their target, budget, or both (Art. 13b). There are a number of preconditions for making the flexibility available to Member States. These include that:

- overall the EU achieves its target,

- Member State exhausted flexibilities from Article 12, and

- Member States reported on measures to protect their carbon sinks or enhance them in their NDCs.

The flexibility is capped at 178 Mt CO2eq. for all Member States, i.e. 50% of the national maximum amounts provided in Annex VII of the Regulation. Different rounds of compensations are foreseen.

- Member States fulfilling the conditions can compensate their debits without additional requirements.

- In case Member States cannot fully compensate their debit, more compensation is granted to Member States that provide evidence that debits occur due to impacts of natural disturbances. However, this round only applies if there is unused compensation available under the mechanism.

- Member States can compensate remaining debits up to another 50 Mt CO2eq of unused compensation from other Member States of the years 2021 to 2030 if they either can provide evidence that these can be attributed to climate change impacts or arise because they have a higher share of organic soils compared to the EU average.

If the demand for compensation exceeds the maximum amount of 50 Mt CO2eq, that compensation will be proportionally distributed among duly justified requests by the Member States concerned

Figure 5: Overview and decision tree of options for the use of flexibilities under the LULUCF Regulation for the period 2021 – 2025.

Source: Own compilation based on LULUCF Regulation.

Figure 6: Overview and decision tree of options for the use of flexibilities under the LULUCF Regulation for the period 2026 – 2030.

Source: Own compilation based on LULUCF Regulation.

How is compliance with the LULUCF regulation assessed?

Compliance with the LULUCF Regulation is assessed in 2027 for the period 2021-2025 and in 2032 for the period 2026-2030. In both years there will be a comprehensive inventory review (see chapter 4.6).

For the first period, Member State and the EU compliance will be assessed against the ‘no-debit’ commitment in accordance with accounting rules

For the second period, Member State and the EU compliance will be assessed against the targets set out in Annex IIa of the LULUCF Regulation. Only after the compliance checks under the LULUCF Regulation have been completed in 2027 and 2032, the compliance cycle under the ESR will start.

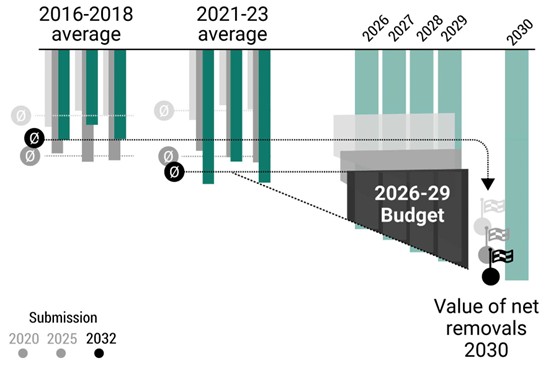

GHG inventory data of different years is relevant for the calculation of Member States’ budgets, the 2030 targets and compliance in both periods. For the calculation of compliance with both the 2030 target (Figure 18) and the budget for the period 2026-2029 (Figure 19), the reviewed GHG inventory data submitted in 2032 will be used..

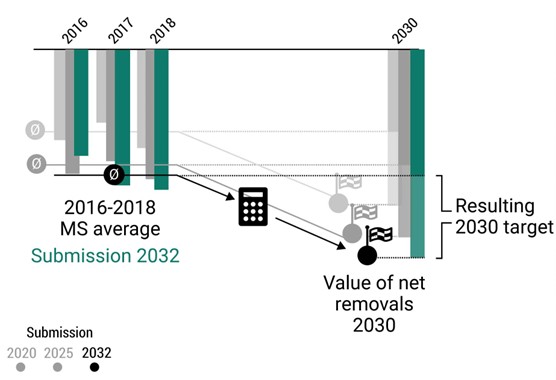

Member States are encouraged to update their methodologies and report using higher Tier methodologies to increase the accuracy and level of detail of their GHG inventories. Such changes can affect the consistency of inventory data used for assessing compliance, national targets and budgets and the Union’s target. Therefore, methodological adjustments, can be applied by the Commission to ensure consistency. Practically, these adjustments reflect the difference of the average data from 2016 to 2018 between the 2032 inventory submission and the one of 2025, in which 2030 targets have been calculated for the linear trajectories (see Figure 7)

Figure 7: Example of Member State target calculation 2030 for compliance in the year 2032\

Source: Own compilation.

Figure 8: Example of Member State target calculation of the budget 2026-2029 for compliance in the year 2032

Source: Own compilation based on LULUCF Regulation.

What are methodological requirements by the LULUCF Regulation?

Under the LULUCF Regulation, targets as well as compliance are based on what Member States report in their GHG inventories. The current methodologies applied by many countries to report emissions and removals need to improve to allow for higher levels of accuracy, precision, and timeliness.

- Under the LULUCF Regulation, targets as well as compliance are based on what Member States report in their GHG inventories. The current methodologies applied by many countries to report emissions and removals need to improve to allow for higher levels of accuracy, precision, and timeliness.

- Conveniently, recent technological developments, for example products from Copernicus Services and digitally collected data under the Common Agricultural Policy are now available and can help Member States in improving their monitoring and reporting of the land sector (see Geospatial Monitoring).

- Using the best available methods, the national GHG inventories will be able to track changes, to reflect policies, and to track whether the targets are met. The best available methods will empower Member States to have a good knowledge of the developments in land sector and to apply measures and policies in a timely and effective manner.

Higher Tiers increase the quality of the calculations, avoiding applying default assumptions for some sectors or subsectors. Using geographically-explicit monitoring of land use changes allows Member States to precisely track what is happening on the field. - Combining high quality datasets in a geographically-explicit framework helps policymakers to have a comprehensive and detailed view of the evolution of carbon fluxes and assess the effect of their policies in a timely manner (see Interoperability)

Which inventory reviews are foreseen by the LULUCF Regulation?

A review consists of checking the quality of inventories. It is periodically conducted at European and international level by teams of experts. Each country’s methods and results are reviewed following the key principles of transparency, accuracy, consistency, completeness and comparability.

- The reviews aim to check for the good application of IPCC guidelines, and that reporting requirements under UNFCCC, and EU legislation are met. The expert review teams examine data, methodologies and procedures used in preparing the national inventory. It pays attention to key categories, areas of the inventory where issues have been identified and recommendations made in previous reviews, progress in the implementation of the planned improvements, or where recalculations have occurred.

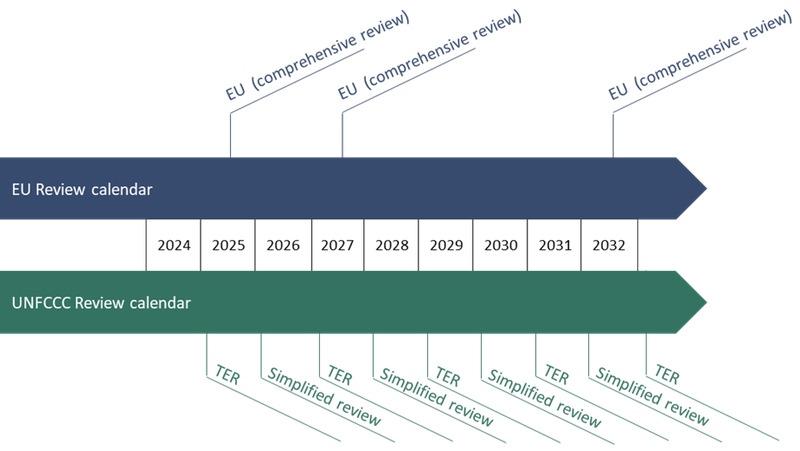

- The updated LULUCF Regulation is accompanied by a specific review process in addition to UNFCCC. A comprehensive review is planned for 2025 to verify the greenhouse gas inventory data up to the year 2023. The average of the years 2021, 2022 and 2023 reported and reviewed in 2025 is considered the basis for setting the linear trajectories. Another comprehensive review is foreseen in 2027 and 2032, before the compliance check against Member States’ targets is carried out.

- These reviews are conducted by the Commission, assisted by the European Environment Agency (EEA). The EEA is responsible for performing quality assurance and quality control procedures in the preparation of the Union GHG inventory, compiling the inventory, and assisting in conducting the inventory review under Article 38 of the Governance Regulation.

According to the Governance Regulation the comprehensive review shall include:

A review consists of checking the quality of inventories. It is periodically conducted at European and international level by teams of experts. Each country’s methods and results are reviewed following the key principles of transparency, accuracy, consistency, completeness and comparability.

Checks to verify the transparency, accuracy, consistency, comparability and completeness of information submitted

Checks to identify cases where inventory data are prepared in a manner which is inconsistent with UNFCCC guidance documentation or Union rules

Checks to identify cases where LULUCF accounting is carried out in a manner which is inconsistent with UNFCCC guidance documentation or Union rules

Where appropriate, calculating technical corrections necessary, in consultation with the Member States.

Figure 9: Timeline for reviews under EU and UNFCCC. TER - Technical Expert Review.

Source: Own compilation.

What are the next steps for implementing the LULUCF Regulation?