| 5EAP objectives for EU (1992-1995) |

Actions achieved |

| Awareness

building |

|

- Economic and fiscal

instruments

|

- New proposal for

Directive on CO2/energy tax

(COM(95)172) - would establish a

harmonised framework for Member States

wishing to apply a carbon/energy tax

(Communication on Environmental Levies

used in Member States, in preparation)

- Amended proposal

(COM(94)147) on excise duties applicable

to fuels of agricultural origin

|

|

| Energy

Efficiency |

|

| Implementation

of PACE, SAVE and national efficiency programmes: |

SAVE

- has supported 25 pilot projects in least cost

planning and demand side management |

- energy efficiency

standards for appliances, products and

vehicles

|

- Three energy

efficiency Directives have been adopted:

hot water boilers, labelling of household

appliances & omnibus Directive 93/76

|

- efficiency standards

for energy technology

|

- Directive proposed on

efficiency of refrigerators and freezers

and draft proposal on least-cost planning

|

| |

Communication

on a Community strategy to reduce CO2 emissions

and improve fuel economy (Council conclusions,

June 1996) |

| Technology

Programmes |

|

| Implementation

of THERMIE and JOULE programmes including: |

- 3rd and 4th Framework

Research Programmes

|

- R&D; of new energy

technologies and promotion and use

thereof

- R&D; on renewables

(ie biomass)

|

|

| Promotional

Programmes |

|

- ALTENER: promotion of

renewable energy

|

- Programme adopted by

Decision 93/500 - promotion of renewable

energy sources (ALTENER). Standards for

biodiesel have been formulated and

support given to pilot projects. Effects

not expected until year 2000

|

| Nuclear

Safety Programmes |

|

- Study on safety and

waste aspects of nuclear energy

|

|

| Transport

user behaviour - development of inter-active

communication infrastructures |

|

- Locking and tracking

systems, electronic home, video

conferences

|

- R&D; efforts

through a range of programmes covering

vehicle-based telematics,

telecommunication and telecommuting. Some

funds from the Drive 2 Programme in

particular are being diverted into

environmental assessment of advanced

telematics

|

|

2.2 Past

trends

Energy consumption and prices

Since the early 1970s energy

intensity1 has decreased mainly due to energy

efficiency improvements and changes in the economic structure

(eg, less heavy industry, less reliance on production of

intermediate goods). This implies a weakening of the links

between GDP, growth in population, and energy consumption.

However, total gross energy consumption in the EU increased

steadily between 1980 and 1990 by about 1% per year on average

and stabilised between 1991 and 1994 (see Figure 2.1). The

rate of increase differs across Member States and is considerably

higher in the more peripheral economies of the EU such as

Finland, Ireland, Italy, Portugal and Spain.

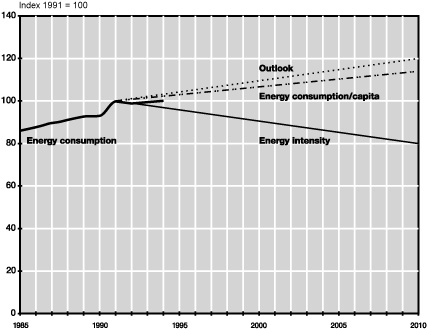

Figure 2.1:

Development of gross energy consumption in EUR15 (the former

East Germany is included from 1991 onwards) Source: Eurostat; EC,

1995

A number of driving forces

influence energy consumption including:

- economic growth;

- increased demand for

transport services;

- low energy prices; and

- growing concern about the

environmental issues.

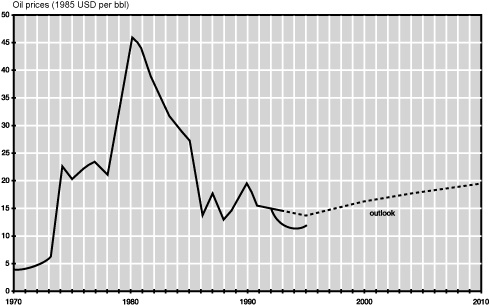

Figure 2.2: World

market oil prices. Source: DEA, 1995; EC, 1995

Oil prices increased sharply

during the 1970s, peaked in the early 1980s and have been falling

gradually since 1980 (see Figure 2.2). The current real

price of energy is now at the same level as the early 1970s. The

price has not been significantly influenced by energy-taxes. The

consumer price of other energy sources was generally made

dependent on the oil price.

Figure 2.3:

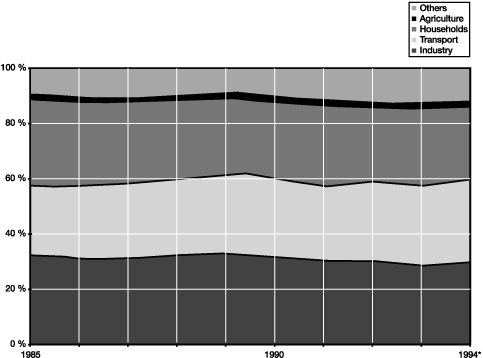

Sectoral final energy consumption in the EUR 15. Source: Eurostat

Energy consumption within each

sector has its own characteristic; the pattern in the households

and the industry and transport are described briefly below (see

also Figure 2.3).

- Energy consumption in industry

in the EU shows a steadily decreasing trend from 1985 to

1994. This evolution corresponds to significant decrease

of the energy intensity of the sector, especially given

that overall industrial capacity increased steadily.

Energy consumption in energy-intensive branches, such as

iron & steel, chemicals, and non-metallic minerals,

was also significantly lower in 1994 compared to 1985.

Sweden is one of the very few countries where energy

consumption by industry increased.

- In the transport

sector, energy consumption grew steadily from 1985 to

1994. In this sector, energy demand has grown faster than

overall economic activity. Therefore, energy intensity in

the transport sector increased by 0.7% pa in the period

1980-1990 (EC-DGXVII, 1994). Also, real prices for

transport fuel dropped, helping to push up fuel

consumption. Significant decrease of the energy intensity

of vehicles was counteracted by an increasing number of

cars, a higher share of larger, more powerful cars in the

transport sector and an increase in kilometres travelled

per capita. Over the period 1980-1990 passenger transport

(in kilometres) by road increased by almost 40%. These

developments are reflected in road transports share

of total energy consumption in the transport sector,

which increased from 79% in 1974 to 83% in 1992.

- In the households and

the tertiary sector, energy consumption grew

slightly from 1985 to 1994, although consumption in this

sector varies with climatic conditions and fluctuations.

Other important factors are population size, number of

households, private income and evolution of the services

sector. It is not possible to give a full split between

both subsectors, but indications are that there has been

growth in energy demand in commerce (supermarkets,

shopping centres, etc) and in households as a consequence

of widespread penetration of household appliances. This

growth in total demand has largely outweighed

technological and other efficiency improvements. In most

Member States, there has been a tendency for demand to

stabilise or decrease over this period; exceptions to

this include former East Germany, Greece and Portugal.

In the electricity sector,

there has been an almost continuous increase in electricity

consumption between 1974 and 1992 by an average of 2.7% pa. In

1992 electricity demand decreased to 1.3% growth as a result of

economic slow down. In 1993 there was, for the first time, a drop

in consumption by about 1%, reflecting economic recession.

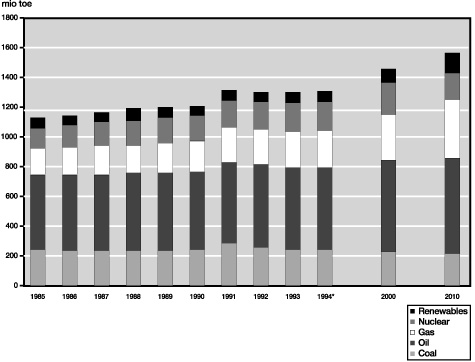

Energy supply

The import dependency for energy

supply has remained stabled during the period 1985-1994: about

45% of the total energy supply was imported (mostly oil).

The mix of fuels in the total

energy supply of the EUR 15 during the period 1985 to 1994 is

shown in Figure 2.4. Oil accounts for the largest share of

total supply (42% in 1994); actual supply from this source has

remained relatively stable since the 1980s. The trend in the

share of energy supply by coal (18% in 1994) has been falling

over the period, while the share by natural gas (19% in 1994) is

slowly increasing. Nuclear power accounts for about 15% of the

total energy supply. The share of renewable energy has remained

stable in the period 1985-1994 at about 5%.

Figure 2.4: Total

energy supply, the former GDR is included from 1991. Source:

Eurostat; EC, 1995

National factors (own energy

sources, direct access to harbours, climate, economic structure,

political preferences, etc) explain the large differences in the

type of energy used across the EU. The new Member States very

much reflect the varying energy source structure for electricity

generation in the EU: Austria has almost equal shares of solids,

oil and gas, and a relatively substantial share of hydro; Finland

is largely dependent on nuclear (45%) as is Sweden (70%).

2.3 Outlook

In 1990 the EC report Energy

for a New Century: the European Perspective identified three

major themes: the changing geopolitical framework, the internal

market and the environment. Subsequent studies in 1992 and 1995

present several scenarios identifying the range of influences at

work that could affect the direction of energy demand and supply

in the longer term. From the latest Commission study -

European Energy to 2020; A scenario approach (EC, 1995) - the

so-called Conventional Wisdom scenario has been used. This

scenario denotes the business-as-usual world,

representing a conventional wisdom view of the most likely

evolution of events2.

Energy consumption and prices

In the period 1990-2010 an average

growth in primary energy consumption of around 1% pa is expected

(see Figure 2.1) (EC, 1995). The same figure also shows

the development in energy consumption per capita. It can be

concluded that the growth in energy consumption will be driven by

production and consumption growth per capita. The growth in

population will be relatively insignificant.

At the time of the 5EAP, the

average growth pa was estimated at slightly less than 1% for the

same period. Thus, despite the promotion and co-financing of

energy conservation initiatives at the EU and national level,

current energy consumption forecasts are virtually unchanged in

comparison with the former projections. Lower energy use in

industry and stable use in the domestic and commercial sector

will be counterbalanced by increased use in the transport sector.

According to the current

estimates, real oil prices would increase by about 60% between

1995 and 2010, and will arrive at the same level as it was in

1990 (see Figure 2.2). It is expected that coal and gas

prices will decline relative to the price of oil.

Unsurprisingly, due to the lack of

economic incentives, future reductions in energy intensity are

likely to be modest. In industry, energy intensity gains must be

considered together with a continuing change in industrial

processing structures. Intensities in the domestic sector are

also expected to decline. Energy intensity is estimated to

decrease by about 1.2% pa to 2010, although the energy intensity

has stabilised in the last 10 years.

One of the EU policy initiatives

with a potential short term impact on the demand side is the SAVE

Programme. This Programme (renewed in 1995) aims to attain a 20%

energy efficiency improvement between 1986 and 1995. Estimates

indicate that only about 10% of the improvement will be achieved.

Recently adopted directives on efficiency for freezers and

refrigerators may yield some results in the immediate future. An

energy/CO2 tax has been suggested by the EC as a

cost-effective instrument for substantial, short-term,

improvements in energy efficiency, taking into account the

responsiveness of energy demand to an increase in prices which

would follow from the imposition of a tax. While an EU wide tax

would be creating a level playing field within the

EU, some Member States (Denmark, Finland, Sweden, Austria, The

Netherlands) have already introduced an energy/CO2. Those

countries which already have such a tax allow exemptions to

industry subject to international competitiveness.

Energy supply

The forecasts in 1995 for EU

internal energy production in the period 1990-2010 show a steady

decrease and the import dependency is expected to increase (from

45 to 65%) (EC, 1995).

The share of total energy supply

accounted for by coal will (further) by around 1% pa due to their

environmental drawbacks (SO2, NOx, CO2) and rapid substitution by natural gas in

power generation, in spite of their competitive pricing (see Figure

2.4). The demand for natural gas is expected to increase

rapidly (about 3% pa). The total shares for coal and gas in 2010

will be about 15 and 25% respectively. The efficiency,

convenience and cleanliness of natural gas has been widely

recognised by residential and commercial consumers. The

prevailing trend in the electricity sector is the penetration of

natural gas combined cycle plants, also built for co-generation

of heat and power (CHP). The industrial market for hard coal and

residual oil is also threatened by competition from natural gas.

The projected further expansion of distribution, particularly in

Denmark, Spain, Portugal, Ireland and Greece, will favour gas

penetration in industry. Nevertheless, price relations between

gas and its competitors are considered decisive. Oil products

remain important for end-use, it is expected that their share in

the market will remain stable.

The share of nuclear power will

hold virtually constant to 2000 and will show a decrease

afterwards (EC, 1995). Although the present share of renewable

energy sources accounts for some 5%, this source has the highest

future growth rate forecast compared to other energy sources and

is expected to account for 7.5% in 2010.

Document Actions

Share with others